Report: Hoosiers paid $29M in 2021 for payday loan finance charges

Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

Capping interest rates on Indiana “payday” loans at a 36% Annual Percentage Rate (APR) could have saved Hoosier borrowers more than $26 million in 2021, according to a recent analysis released by the Indiana Community Action Poverty Institute.

Loans during that period averaged just $386 but payday lenders collected over $29 million in finance charges.

“Payday lenders drain millions from Hoosiers, their families and their communities every year,” said Andy Nielsen, the Institute’s senior policy analyst, in a statement. “Payday loans are inherently flawed: they violate anything close to a true borrower-creditor relationship in exchange for a one-sided agreement that fuels a debt trap for vulnerable borrowers.”

Nielsen called for lawmakers to step in and better regulate the small loans market to protect low-income Hoosiers who might utilize payday lenders.

The report criticized lenders, many of which are headquartered out of state, for taking money out of local economies and luring Hoosiers into “a debt trap.”

“Because of a lack of strong consumer protections, financially vulnerable Hoosiers are threatened by a system that pulls them in and keeps them there — a cycle that they will likely struggle to leave,” the report said. “Consumer-friendly policies that prevent a debt trap and provide more affordable credit through strong rate caps would have a demonstrable impact on our state and the lives of Hoosiers.”

Payday lending in Indiana

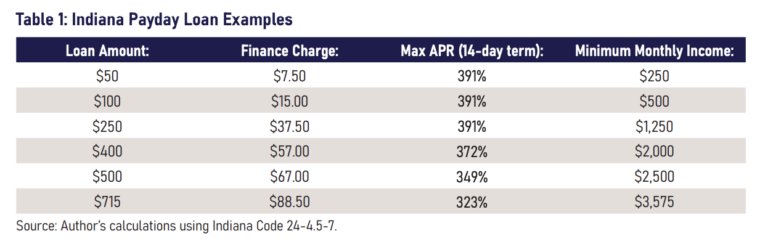

The state does maintain some restrictions on payday loans, or small loans in the Indiana code. The principal loan amount can range from $50 to $715 but mustn’t exceed 20% of a borrower’s gross monthly income. A borrower can only have two outstanding loans and, in 2023, those outstanding loans cannot exceed a combined $715.

Additionally, the minimum term must last 14 days and after six consecutive loans, a lender must wait seven days before offering a new loan.

Lastly, charges are limited to 15% for the first $250 borrowed; 13% for loans between $251 and $400; and 10% for a loan over $400.

But advocates decry the loans as “predatory,” noting that lenders don’t access a borrower’s ability to repay the loan.

Unlike other loans, payday loans are exempt from the state’s criminal loansharking limit of 72% APR. Payments on a loan don’t build up a person’s credit score but failing to pay appears as a collection on a borrower’s credit report.

Loans sent to collectors also don’t count toward the maximum number of loans or total borrowing limit, meaning borrowers can be enticed to take out a new loan. A 2019 report from the Institute found that 60% of borrowers borrow the same day they repay an old loan.

“While borrowers are entitled to a no-cost extended payment plan after their fourth loan, this feature does not appear to provide a meaningful protection against a debt trap,” the report said.

Payday lending and suggested reforms

Lenders, whether based out of a physical location or an online entity, must register with the Indiana Department of Financial Institutions. According to the report, there were 17 registered payday lenders in 2021 with 161 branches — down from 32 registrants with 285 branches in 2016, a 46% decline in lenders and a 43% decrease in physical locations.

Payday lending had a “precipitous drop” in 2020, likely due to enhanced federal support during the early days of the COVID-19 pandemic. Those benefits include stimulus checks, rental assistance and more robust unemployment insurance. Lending recovered slightly in 2021 but dropped again shortly after Congress restructured the child tax credit to be larger and paid monthly.

Despite those changes, 555,940 small loans totaling $214.7 million were opened during 2021, with advance fees of approximately $29.2 million.

The Institute offered several alternatives for Hoosiers seeking short-term loans, noting that some banks and credit unions now offer small loans.

Other options may include:

- Employer programs to take a paycheck advance

- Employer partnerships with community loan centers offering loans at 18% interest, with 3% up front

- State grants for military service members and veterans

- Local Area Agency on Aging, for borrowers who are either disabled or over 60

- Calling 211, a state helpline that can connect someone to various ogranizations

- Local Community Action Agencies

- Local township trustees

The Indiana Capital Chronicle is an independent, not-for-profit news organization that covers state government, policy and elections.