Rebounding banks see tailwinds ahead

Subscriber Benefit

As a subscriber you can listen to articles at work, in the car, or while you work out. Subscribe Now

It’s good to be a banker these days.

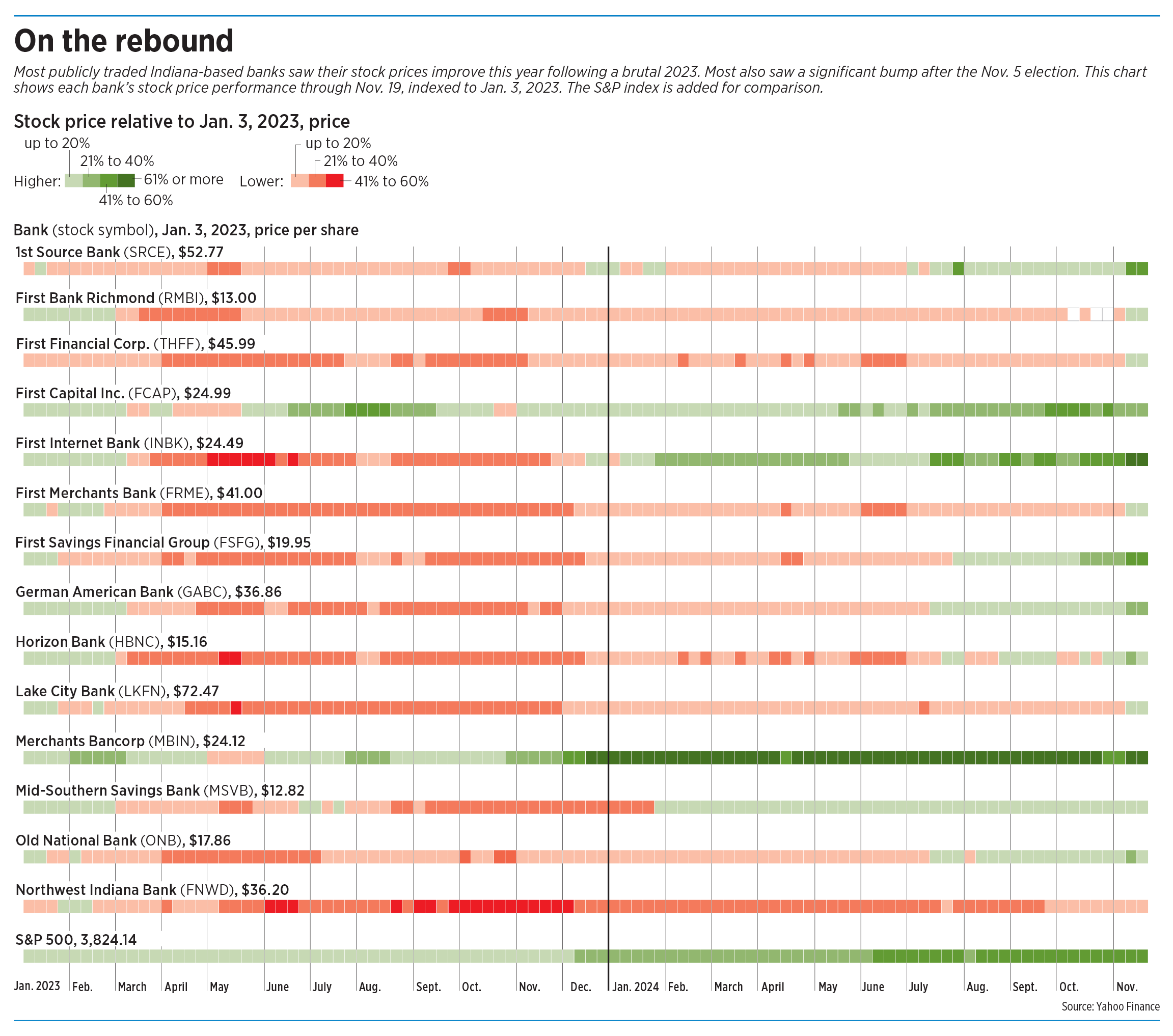

After a tough 2023, when a variety of factors sent bank stock prices plummeting in Indiana and beyond, most publicly traded banks in the Hoosier state have seen at least a partial rebound in their stock prices this year. And looking ahead, banks see even more reasons for optimism.

“Sentiment is somewhat euphoric,” said Nate Race, who covers the banking industry as a Chicago-based senior research equity analyst at investment bank Piper Sandler Cos. “It’s a really favorable setup for the industry going into the next year.”

Race and Indiana banking executives say multiple factors, including the recent drop in interest rates and the outcome of the presidential election, add up to good news for the banking industry.

Among Indiana’s publicly traded banks, Fishers-based First Internet Bank has seen the most dramatic turnaround in stock price.

First Internet stock was trading above $25 in early 2023. The price began to drop that March, closing below $11 per share on several days in May. The bank’s share price had rebounded by the end of 2023 and continued to gain this year, closing at $42.18 on Nov. 25.

“We took a hell of a punch last spring and kind of got knocked down quite a bit,” said First Internet CEO David Becker.

Banking took a hit last year when several bank failures cast a pall on the entire industry, Becker said, and two years of rapidly rising interest rates put a squeeze on profitability. Another factor specific to First Internet, he said, was that a big loan went bad. The bank took a partial charge-off of $4.7 million in the first quarter of 2023 to account for that loan.

In contrast, Becker said, “every indicator’s going up right now.”

Reasons for optimism

One big positive for banks right now is the recent drop in interest rates—and the expectation of further cuts.

The Federal Reserve raised interest rates a total of 11 times in 2022 and 2023, taking the target federal funds rate from less than 1% in March 2022 to a high of 5.5% in July 2023. The Fed has cut its target rate twice this year, reducing it to 5% in September and to 4.75% earlier this month.

Speaking to a group from the Central Indiana Corporate Partnership in Indianapolis last week, Federal Reserve Bank of Chicago President Austan Goolsbee said he favors additional reductions. Goolsbee is a member of the Federal Open Market Committee, which meets every six weeks to discuss monetary policy and decide whether to adjust interest rates.

For First Internet, Becker said, every quarter-point drop in interest rates translates to $5 million in additional income over a 12-month period.

Since banks earn money from the interest they charge on loans, it might seem counterintuitive that a drop in interest rates is good news for banks.

But banks also pay interest to customers on products like certificates of deposit and money market accounts. For example, Becker said First Internet has CDs maturing now that are paying 5.15% interest. But the interest rate the bank is currently offering for new CDs is 4.2%.

Another way the reduction in interest rates helps: It can both spur demand for loans and increase the likelihood that those loans get repaid.

“The easing of interest rates takes some of the pressure off of credit concerns,” said Mark Hardwick, CEO of Muncie-based First Merchants Bank.

About 75% of First Merchants’ loan portfolio is made up of variable-rate loans; if interest rates go up, so can a borrower’s monthly payments. And a higher payment means a higher likelihood that the borrower will have trouble making those payments. The reverse is true when interest rates drop.

For the same reason, lower interest rates can also convince would-be borrowers to get off the fence and take that loan.

Jim Ryan, CEO of Evansville-based Old National Bank, said loan demand typically goes up when interest rates drop.

Regulatory relief

The outcome of the presidential election, which will put Donald Trump back in the White House and fellow Republicans in the majority in both houses of Congress, gives banks another reason for optimism.

“The Republican Party is [as of January] pretty much in control of everything,” Becker said. “Their game, particularly on financial services, is less regulation.”

Most publicly traded Indiana banks saw their stock prices jump significantly immediately after the election, and those prices have remained elevated.

That pattern was also true for banks in general, Race said. On Nov. 6, the S&P 500 closed 2.53% higher than it had the day before. Bank stocks as a group were up 13%.

To Hardwick, the immediate jump in stock prices suggests that investors—particularly fund managers who had been skittish about bank stocks—decided to get back in the game.

“I feel like they were ready to go and expecting more rate cuts that would make for a more optimal interest-rate environment. And then the election happened, and they all jumped in, and they were poised and ready to go,” Hardwick said. “There’s just a belief that under the new administration, there’ll be less of a regulatory burden on banks.”

First Merchants stock, which had a share price above $40 in January 2023, saw its value tumble shortly afterward, not fully recovering until this month. The bank’s stock closed at $43.41 Nov. 6, up from a closing price of $37.49 the previous day. The bank’s closing price Nov. 25 was $44.97.

Warsaw-based Lake City Bank’s stock performance has been similar to that of First Merchants—languishing for the better part of two years until this month.

Lake City’s stock, which closed at $72.47 on Jan. 3, 2023, began to fall that month, closing below $50 per share on many days last year.

The bank’s stock price had begun to rebound by the end of 2023, with closing prices creeping higher this year. The big boost came on Nov. 6, when Lake City’s stock closed at $73.94 per share, up from $66.53 just one day earlier. The bank’s share price has held above $70 since then.

Lake City’s CEO, David Findlay, said he shares the view that the incoming Trump administration will be softer on banks than the Biden administration has been.

As one example, Findlay said he anticipates a shift at the Consumer Financial Protection Bureau, which he characterized as having been “very critical of traditional banking practices, particularly at the larger banks in the country.”

Among its other actions, the CFPB has been active in its opposition to things such as bank overdraft fees, which the bureau has repeatedly described as “junk fees.”

“That’s just a polarizing statement on a banking product that our customers … appreciate having and are thankful for the existence of,” Findlay said.

Last week, in fact, The Washington Post reported that Trump and Republicans in Congress are “weighing vast changes” that would limit the CFPB’s powers and funding.

The banking industry also perceives that the Trump administration will make bank mergers-and-acquisitions activity easier, which is another positive from the industry’s point of view.

Nathan Stovall, a banking analyst with S&P Global Market Intelligence, said bank deals have been harder to close over the past few years because regulatory scrutiny has drawn out the approvals process. And, he said, “the longer it takes to close, the more risk that’s associated with it.”

Trump’s “America first” stance, and the increase in domestic manufacturing that could happen as a result, might also be good news for banks. Manufacturers adding sites or expanding operations might be in need of loans or other financial services that banks can provide, Race said.

The mere fact that the election is behind us is also a positive, Old National’s Ryan said.

“I think clarity on the election outcome is always helpful, regardless of the outcome,” he said. “Any kind of political uncertainty will have people pause.”